Restricted Stock Unit (RSU)

Understanding RSUs

RSUs (Restricted Stock Units) are a form of stock compensation used by companies to reward their employees. Unlike stock options, which give employees the right to purchase shares at a given price, RSUs represent a company’s promise to transfer a certain number of shares to the employee at a specific future date or once certain conditions are met. These conditions may be tied to the employee’s length of service (for example, staying with the company for a certain number of years), specific performance goals, or other criteria.

Once these conditions are met, the RSUs are “vested”, meaning the employee can take possession of them. At this point, RSUs are typically converted into ordinary company shares, which the employee can then keep or sell according to their preferences. It’s important to note that employees often have to pay taxes on the value of the shares when they vest.

RSUs are a commonly used tool to attract and retain talented employees, particularly in sectors such as technology where competition for skills is intense. They also help better align employee interests with those of the company, since the value of RSUs generally increases with company performance.

Taxation

Since RSUs are shares, the ultimate values are unknown when the RSU plan is created. Depending on the share value at the time of vesting, your income could be higher or lower than initially expected. Your taxation would be similarly modified.

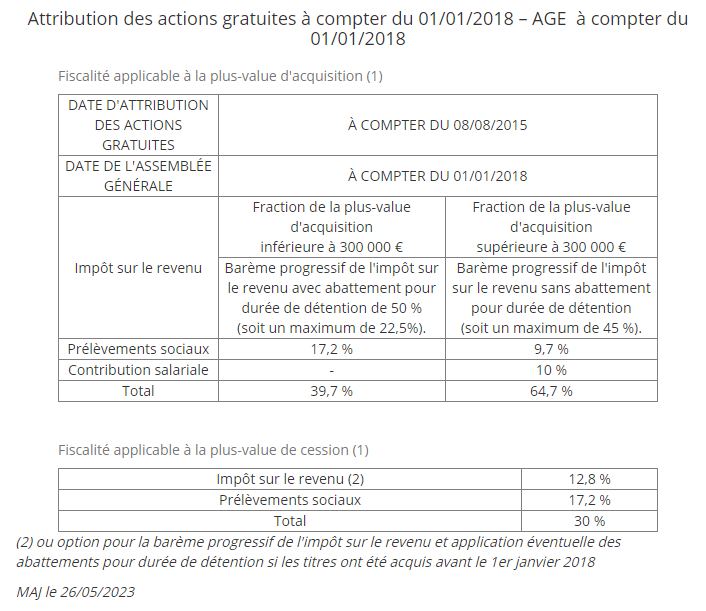

There are two RSU plans, the so-called qualified plan and the non-qualified plan. Depending on which one your company has adopted, you will benefit from a more or less advantageous tax regime.

To know which regime your company has adopted, you simply need to check whether there was any withholding tax.

- If withholding tax = non-qualified plan, so no advantageous tax regime

- If no withholding tax = qualified plan with advantageous tax regime

Below is an example and calculator for a qualified plan.

A Concrete Example

Imagine a new employee joining a company with a compensation package including €100,000 in RSUs, in addition to an annual gross salary of €50,000. To determine the number of share units to be granted, the company calculates the average closing value of the share during the employee’s arrival month.

For simplicity, let’s say this average value is €100. The employee will therefore receive 1,000 share units, because:

- €100 per unit * 1,000 units = €100,000

Following the table above, the employee will benefit from a 50% reduction on the €100,000 in shares:

- 50% of €100,000 = €50,000

- Let’s assume your marginal tax rate (MTR) is 41%. (you can calculate your MTR on the associated page)

- Your annual gross salary of €50,000 would give approximately €33,000 of taxable income (after 10% deduction).

- Adding the €50,000 from RSUs, your taxable income would be €83,000.

The taxation would then be calculated as follows:

- €51,092 taxed at 30%: €15,328

- €4,430 taxed at 41%: €1,816.3

- Social charges of 17.2% on €83,000: €14,276

- This gives a total taxation of approximately €31,420.

Capital Gains Tax

If the share value increases, your potential gains will also increase. Let’s take the example where the share price goes from €100 to €120. Your gain would be:

-

(€120 - €100) * 1,000 shares = €20,000

For this capital gain, you’ll have the choice between the 30% flat tax or integration into taxable income. Most of the time, the 30% flat tax is more advantageous. -

30% of €20,000 = €6,000

RSU Tax Calculator (Qualified Plan)

Non-Qualified Plan

However, a non-qualified plan doesn’t provide any particular tax advantage. The taxation will be treated as salary and will be calculated in two steps:

-

Vesting Gain This is the initial amount of RSUs that was granted to you at the beginning. This will correspond to the percentage that has been unlocked, for example 25% for the first year. This will result in the payment of social security contributions as well as income tax which will again depend on your MTR.

-

Capital Gain No secret here, this will be the difference between the price at the time of share acquisition and the sale price, which will be subject to the 30% flat tax.

You can visit this page which explains in detail how it works => RSU (Restricted Stock Unit) Taxation

Sell to Cover (Non-Qualified Plan)

The “Sell To Cover” mechanism plays a crucial role in RSU (Restricted Stock Units) management. It involves selling a portion of the vested RSUs to cover the tax obligations generated by them.

The procedure may vary by company, but generally, at each vesting date, when RSUs become the employee’s property, the employer automatically sells a portion of the shares to satisfy the taxes due. This sale is based on the value of the RSUs that were initially granted and are unlocked at the vesting date.

During this operation, the employer sells enough shares to cover the taxes. At the end of the month, during payroll, the proceeds from this sale are used to pay the taxes, and any excess from the sale is returned to the employee.

As for the remaining shares after this operation, they belong entirely to the employee, without additional tax charges.

Let’s take an example to illustrate this process:

- A new employee receives €100,000 in RSUs as part of their compensation.

- The RSUs are structured so that 25% vest each year.

- Thus, at the end of the first year, the “Sell To Cover” mechanism is activated to cover taxes related to the 25% of vested RSUs.

- The employer sells a portion of the shares, uses part of the proceeds to pay taxes, and returns the excess to the employee.

- The remaining shares are transferred to the employee, free of any additional tax obligations.

Vesting (Non-Qualified Plan)

Unlike stock options, which employees have the option to purchase, RSUs are directly granted by the employer. However, there’s a catch: they’re not immediately available. This is what we call the “vesting” period.

How Does Vesting Work? RSU vesting typically follows a predefined schedule that encourages long-term loyalty and commitment to the company. Let’s take a common example: you might be able to unlock 25% of your RSUs after the first year of employment, followed by additional 1/4 every quarter for the next three years. In total, it will take you four years to unlock all the RSUs that were granted to you.

What Happens If You Leave the Company Earlier?

The answer is simple but harsh: you lose the unvested RSUs. This means that if you leave the company before the end of the vesting period, you will only benefit from the RSUs already vested up to that point. The unvested units will return to the company.

Tips

Exchange Rate

RSUs are particularly favored by American technology companies as a tool for employee retention and motivation. However, one detail deserves special attention for those working outside the United States: currency.

Watch Out for Exchange Fees

Since RSUs are often valued in US dollars, it’s crucial to consider exchange fees when cashing in these units.

A tip to minimize these costs is to transfer the funds to a bank account offering competitive exchange rates and reduced fees.

Some online banks, like Revolut, offer advantageous exchange rates with minimal fees, which can be economically wise when receiving the value of your RSUs.